Tokenized Startups

Restoring Access to Pre-IPO Companies

Public markets for the world’s fastest-growing tech companies don’t work like they used to. 30 years ago, Amazon went public at a $438 million valuation, three years after its founding. Netscape IPO’ed eighteen months after it was created. But today, the fastest-growing companies – Stripe, SpaceX, OpenAI, Ramp – routinely stay private for a decade or more. The exposure to a company’s highest-velocity growth years, once accessible to public investors, has been quietly hijacked by private capital at ever-higher paper marks.

“If I were using cynical words, I’d say [venture capital] hijacked the growth years of early IPO companies. Amazon went public below a billion in market cap. It’s hard to fathom that today.” – Bill Gurley [1]”

The market has responded with ad-hoc fixes: SPVs, secondary platforms, tender offers, and other instruments designed to quench investor thirst for growth-stage venture assets. But these are patches, not solutions. What investors may really want is what tech IPOs used to promise thirty years ago: broad, liquid exposure to generational companies with venture-scale upside.

Tokenized venture assets could be part of the answer. This piece explores how tokenized startups might bring these disjointed markets back into equilibrium across three questions: (1) why now is the right time for tokenized startups, (2) what does the landscape for tokenized startups look like, (3) what are the key opportunities, challenges, and unresolved tensions standing between this category and scale.

Part I - Why Now for Tokenized Startups?

Tokenized startups sit at the crossroads of three converging trends: (1) the explosion of ad-hoc instruments like SPVs as the de facto liquidity mechanism for generational tech companies, (2) the rapid growth of tokenized real world assets (RWAs), spanning money markets to public equities to commodities and more, (3) the breakdown of the “token-equity” consensus, where project tokens have increasingly become second class citizens relative to venture equity exposure.

1.1 - The Rise of SPVs

A decade ago, SPVs were a niche instrument - a way to pool capital outside of traditional venture or public financing structures [2]. But over the last two years, they’ve become a critical part of capital strategy, with platforms like AngelList, Carta, and Assure making it easier than ever to spin up SPVs for specific opportunities and companies [2]. In particular, secondary SPVs have grown by over 545% over the last two years, with more than a 10x in capital raised [3]. These ad-hoc market structures have captured significant market growth - Hiive’s weighted basket of the Top 50 secondary assets have seen a 49.1% growth in 2025, significantly outperforming the S&P 500 [4]. It is a sign that investors are using ad hoc private-market structures to recover functions that public markets used to perform more cleanly: access, liquidity, and price discovery. As companies stay private longer, SPVs have become one of the main substitutes.

1.2 - RWAs, Tokenization, and Perpification of Everything

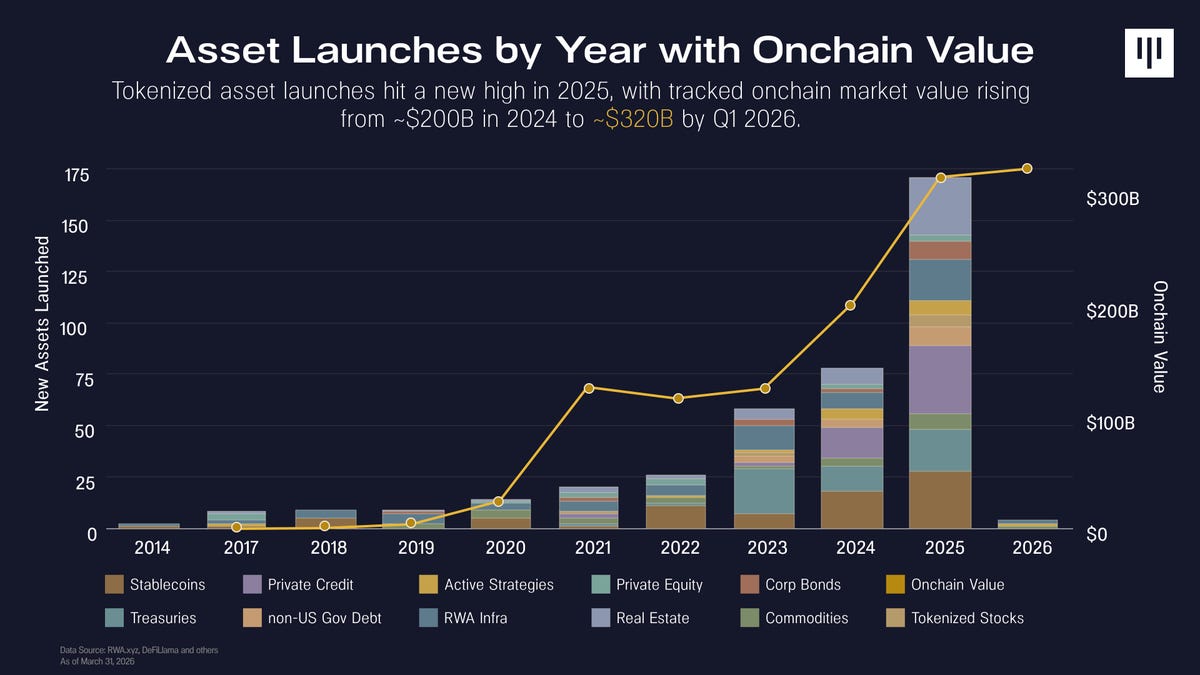

The second trend is the rise of tokenization and perpetual markets across a variety of asset classes. In Q1 2026, onchain RWA value has reached ~$320B [5]. While the largest RWA asset class continues to be US Treasuries (which can act as collateral for stablecoins), there has also been a significant rise in asset classes like commodities, stocks, and asset-backed credit like Figure’s home equity loans (HELOCs) [6]. As RWAs gain adoption, we can see the tokenization supply chain mature - from issuers to custodians to regulatory frameworks.

In parallel, perpetual futures, or “perps” have grown tremendously over the past 2 years, with the rise of perpetual decentralized exchanges (perp-DEXes) like Hyperliquid. Compared to dated derivatives, perps do not have expiry dates, which allow for better practical execution perspective, simpler to understand from a risk perspective, and natively 24/7 [7]. Projects like TradeXYZ have also expanded perps beyond pure crypto pairs (such as BTC-USDC) to other asset classes, including US and Korean stocks, commodities, and equity indices by offering a standardized way to create new perpetual markets in conjunction with HIP-3 [8].

1.3 - The Breakdown of the Token-Equity Consensus

The third growing trend is the value-accrual dilemma between tokens and equities. DeFi project tokens, such as UNI and AAVE were issued to explicitly not represent equity to address regulatory concerns. This created a “token-equity consensus,” where project tokens were supposed to be synthetic instruments giving owners “governance rights” over parts of a protocol, with fee collecting promises as a means to accrue value. However, this created a two-tiered system, with zero-sum value accrual, and tokenholders became like second class citizens to equity holders. This problem became clear with recent events like the Aave DAO vs. Labs standoff and the contentious Circle-Axelar acquisition, where tokenholders interests’ were subsumed to equity interests. All this prompts a rethinking of the existing “token-equity consensus” – how can we design tokens that better represent a project’s upside?

The convergence of these three major trends may pave the way for the rise of “tokenized startups”: tokenized exposure to a company with venture-scale upside, allowing the general public early access to generational companies the way the public markets used to. In this way, tokens become a re-architecturing of the traditional IPO, allowing broader public access to the hottest generational companies.

Part II - The Landscape of Tokenized Startups

2.1 - Design Approaches and Volumes Today

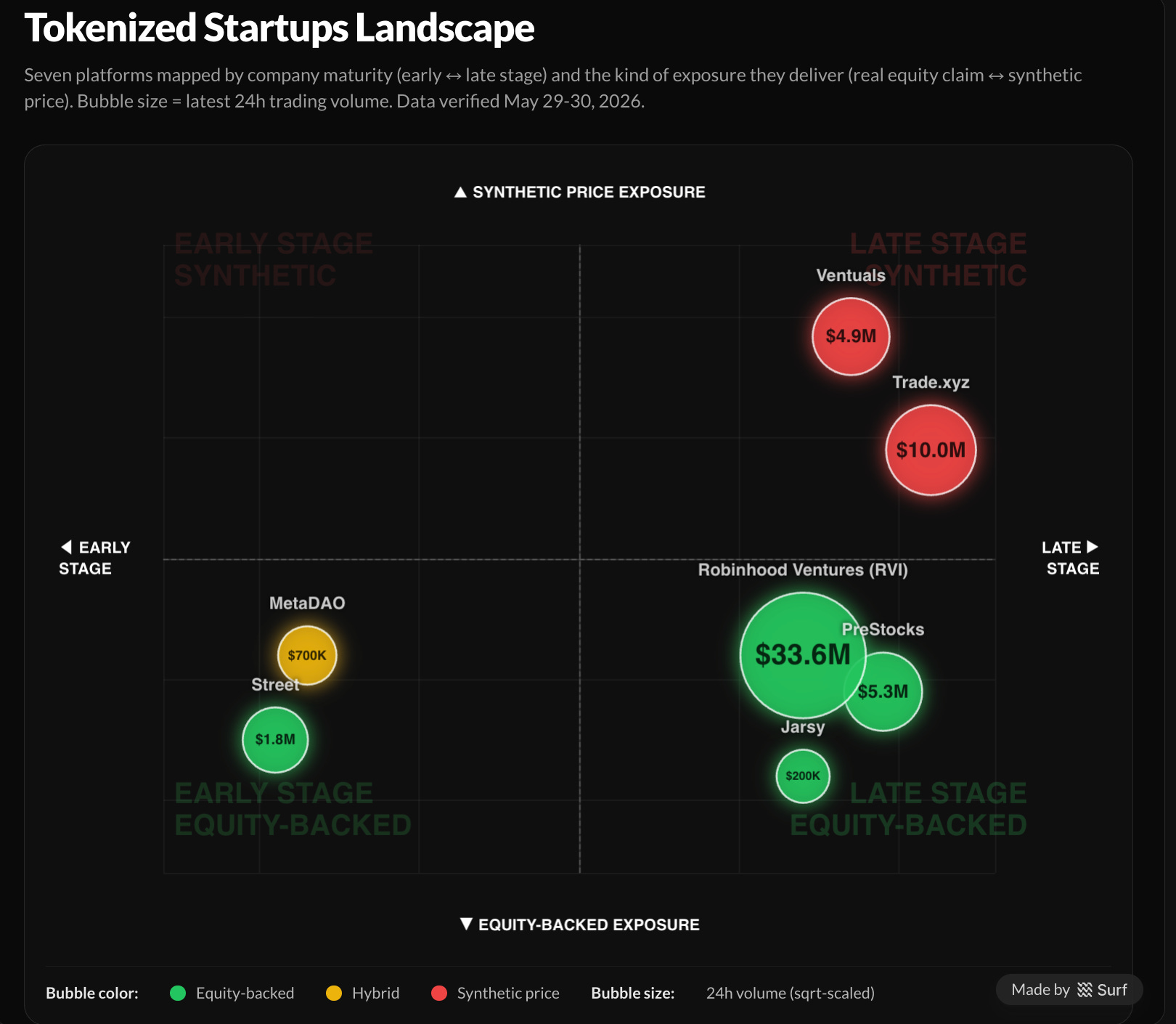

Landscape of Tokenized Startups. Made with Surf AI.

Today, there are a variety of approaches and designs to tokenized startups along two main dimensions - exposure mechanism, and startup stage. The exposure mechanisms of tokenized startups ranges from an equity-holding SPV instrument (such as PreStocks), to Closed End Funds with company equity access (such as Robinhood Ventures), to pure perpetual futures that provide only price exposure with no underlying equity ownership (such as TradeXYZ and Ventuals). The startup stages range from early-stage companies (such as MetaDAO’s platform) to growth stage assets and household pre-IPO names such as SpaceX, Anthropic, and OpenAI.

Mapping out the major players in the space and their scale (24hr trading volumes as of May 30), we notice several distinct patterns. Firstly, the biggest trend is that late-stage (esp. Pre-IPO startups) dominate early stage platforms by over 10x. In particular, users seem to gravitate towards exposure to Pre-IPO names, such as SpaceX, Anthropic, Anduril, and OpenAI, regardless of the platform offering these assets.

Secondly, equity-based tokenized startups, (such as via Robinhood Ventures and PreStocks) generally see more trading volume than their perps counterparts. Part of this could be simply skewed by Robinhood’s distribution as a platform, as well as TradeXYZ’s one-startup-at-a-time rollout of IPO perps. Notably, TradeXYZ’s IPO perpetual for Cerebras Systems was extremely successful, seeing over $30 million in daily volume and offering accurate price discovery within < 3% of the IPO price [9].

Thirdly, all platforms within this landscape see a power-law concentration effect, where the platform’s volume gets dominated by < 3 assets. MetaDAO, for example, has its trading volume dominated by META, Avici, and Umbra. Street has its volume dominated by KLED. TradeXYZ currently (as of May 30, 2026) only offers SpaceX via SPCX-USDC, and SpaceX also contributes to about half of PreStock’s weekly volume. This massive power law effect could indicate that for most platforms, traders are much more loyal to the brand-name high quality assets rather than the underlying platform itself.

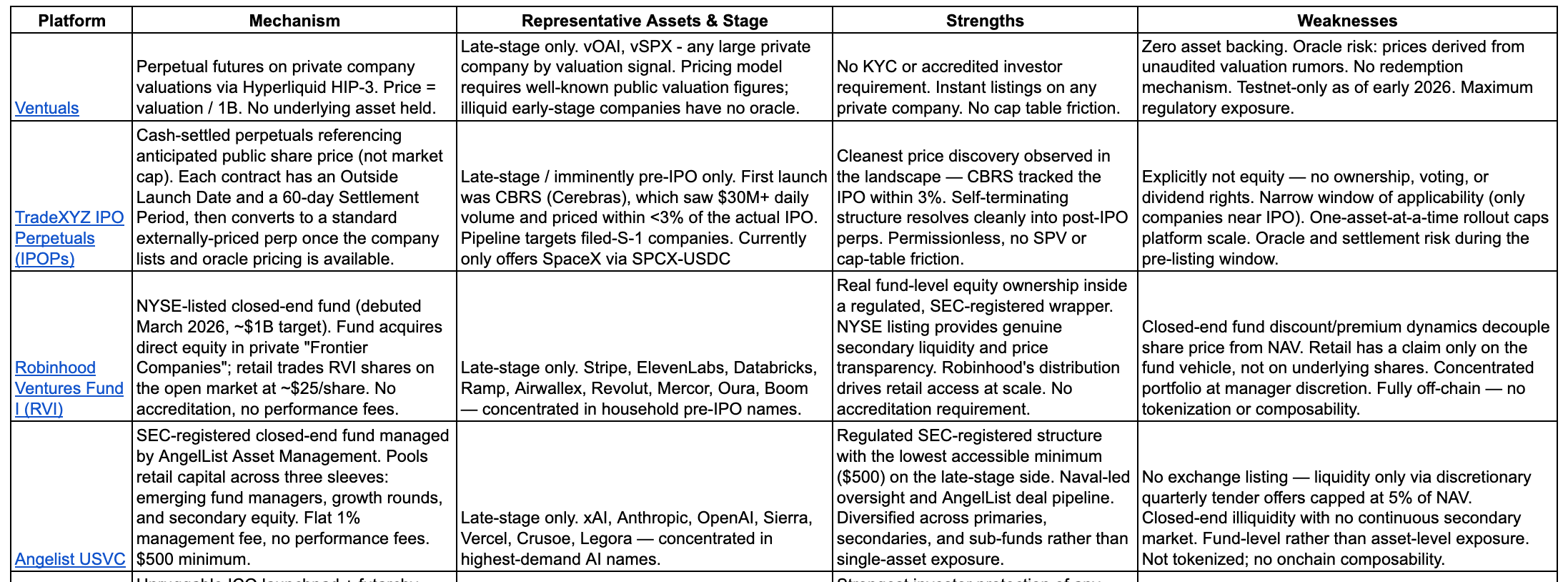

2.2 - Project Design Architectures

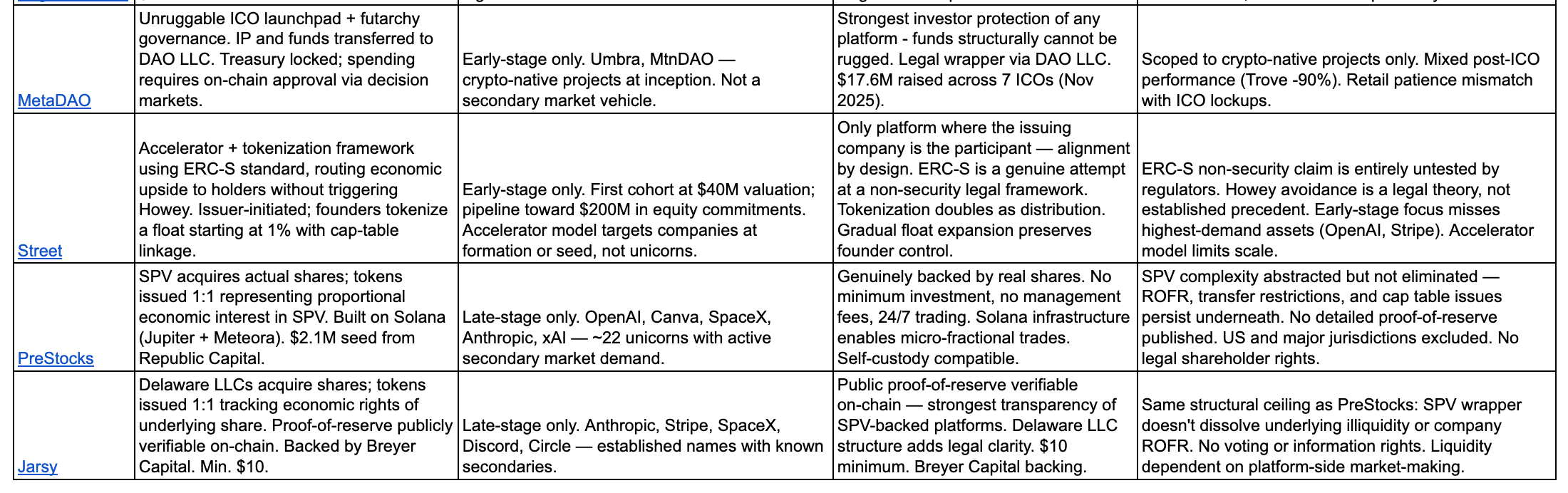

We can also dive deeper to examine the individual projects within this landscape map more carefully to understand the various design tradeoffs in this space, ranging from perp exposure to SPV backed equities.

Note: Platform comparisons and characterizations in this analysis represent the opinion of the author based on publicly available information as of 5/30/2026. Descriptions of platform strengths and weaknesses are not investment recommendations.

Part III - Challenges and Opportunities for Tokenized Startups

Tokenized startups are still in their infancy today, and the design space is filled with many opportunities and challenges [10].

3.1 - Equity Transfer Consent and Team Alignment

One of the most pressing questions right now for (spot-based) tokenized startup platforms is whether or not these projects actually work with or against the interest of the founding team of the company - especially as platform trading volumes are disproportionately concentrated 1-3 quality assets.

This is especially true for high-profile pre-IPO companies such as SpaceX, Anthropic, and OpenAI where much of the pre-IPO demand and volumes takes place. Without it, the company can publicly announce opposition to the tokenization, leading to sales being voided and subsequent crashes in token value, as seen with Anthropic opposing secondary SPVs and OpenAI opposing Robinhood’s stock tokens [12].

Generally speaking, growth-stage companies have four distinct incentives to pursue an IPO: (1) access to capital on public markets, (2) real-time pricing, (3) liquid exits for founding team and investors, and (4) prestige signalling.

Today, the proliferation of growth-stage “megafunds” provide the hottest startups with an extremely robust and plentiful funding environment - often at extremely generous valuations [11]. This dynamic diminishes incentives (1) and (2) for growth-stage companies to go public: they no longer need to turn to public markets for funding, and real-time pricing runs the risk of correcting prices downwards.

Thus, in today’s funding environment, a hot growth-stage startup will only go to public markets if there is a significant amount of early stage employees and investors wanting immediate liquidity (eg. Facebook’s 2012 IPO), or as a “coming-of-age” prestige badge.

For a spot-based tokenized startup platform to have board blessing for direct share access in the current funding environment, the latter two incentives carry much more weight. Traditional secondary brokers like Forge and Hiiv cater more to the liquidity incentive, whereas high-profile Closed-End Funds such as Robinhood Ventures and USVC arguably cater to the prestige incentive.

Nonetheless, in addition to these traditional IPO incentives, there is also a set of emerging designs, such as tokenized startup baskets, tokenized accelerator models, and tokenized community offerings that can solve this adverse incentive problem:

Tokenized startup baskets refer to tradable portfolios of growth-stage startups rather than single tokenized companies. This is the route that Closed-End Funds such as Robinhood Ventures offer. This mechanism could enable the liquidity and prestige, and potentially capital access incentives, while mitigating the downward-repricing pressure of the “real-time pricing” of public pricing by using a NAV multiple (somewhat similar to DATs).

Tokenized accelerator models apply the traditional accelerator and incubation model (eg. YC, HF0, South Park Commons) in helping startups grow from 0 to 1 in exchange for their blessing to tokenize shares. We see launchpads such as Street and MetaDAO effectively offering this model – they solve the founder alignment issue by being on the founder’s side and actually helping the founders grow.

Tokenized community offerings are perhaps the most interesting and exploratory model for tokenized startups. As shown during the Uniswap airdrop in 2020, tokens can act as great incentives for everyday users to use the product on a daily basis. When done well, a token airdrop reduces CAC by subsidizing organic user activity, boosting project marketing, and increasing user satisfaction, particularly for consumer-facing projects. Revolut, for example, did a community equity round that raised $1.3M from early users at a $40M valuation. This doubled as marketing, turned users into owners and evangelists, and those early backers have seen 400x returns. However, token airdrops can also be a double edged sword - many crypto project airdrops have been plagued by airdrop farming, accusations of insider allocations, and instant selling pressure.

3.2 - Non-US Jurisdictions

Another route around the founder alignment problem can just be to go global. Much of the current discussion around tokenized startups (and trading volumes) takes a US-centric approach, concerning the hottest US companies (such as SpaceX, Anthropic, OpenAI), and assuming a US IPO. But both the public and private capital markets in the US already serve growth-stage companies extremely well, which makes the additional benefits of tokenized offerings hard to justify for companies.

However, this is not necessarily true for other geographies, where the local capital markets may be inefficient and not provide the best liquidity or pricing for the fastest-growing companies. Wise, for example, originally listed on the London Stock Exchange in 2021. However, in May 2026, it shifted its primary listing to the US NASDAQ, as it believed the move could draw on more liquid markets, have broader access to both retail and institutions, and have a more generous valuation multiple [14].

This geographical divergence in valuations and capital access is also evident in the difference in valuation multiples between US AI companies and their Chinese counterparts. Whereas US AI leaders routinely have P/S ratios of 15-40x, Chinese AI companies see much more conservative ratios of closer to 5-15x. This discount may partially be attributable to capital access – the Chinese capital market is generally much harder to access than the US markets. This geographical valuation arbitrage becomes particularly interesting as different parts of frontier supply chains – such as for AI, robotics, semiconductors, biotech – remain spread across the world, with relevant companies listed across markets in Asia and Europe.

Yet, despite this structural advantage that non-US jurisdictions have in tokenized startups, currently there is limited empirical experiments and volumes, possibly due to the difficulty in sourcing high-demand startups willing to experiment with their cap table, as well as complications with local regulations around foreign investments and tokenization. A particularly interesting non-US market to watch for tokenized startups is South Korea. South Korea has (1) several national champions such as Samsung and SK Hynix in the AI supply chain with global investor demand, (2) a new legal framework for “stock tokens”, (3) brokerages actively paying attention to pre-IPO investments, and (4) more crypto investors than stock investors. Indeed, this may be part of the reason why projects like TradeXYZ actively started to list perpetuals on Korean stocks.

One of tokenization’s greatest strengths is in its geographical arbitrage capability, able to provide a global audience ground-floor access to companies from all over the world. Tokenized startup platforms - with their global liquidity base and potential accessibility to a broader set of retail and institutional investors could very well become part of the uplisting strategy of the next generation of the Wise’s of the world – fast growing companies outside of the US that do not have as robust local capital markets.

3.3 - Price Discovery Design for Perps

The other route for tokenized startup platforms is the perp playbook. If all you have are synthetic instruments that do not represent underlying equity, then there is nothing a board can actually void. This sidesteps the need for team access and board consent. However, synthetics trade legality for a price discovery problem.

Existing perps markets – such as perps for crypto tokens, stocks, and commodities – typically assume a liquid spot market and reliable price oracle to manage funding rates and synthetic prices. However, private startups by definition do not have liquid public markets. The closest that you get are tender offers and secondary purchases, which platforms like Ventuals use to anchor their funding rates. However, these are often unreliable, and routinely underprice pre-IPO assets. On Ventuals, for example, the funding rate runs about 15% annualized within 5% of the oracle, and beyond that climbs an exponential curve, creating punitive fees for longs.

TradeXYZ takes an opposite approach, relying on an oracle-less price discovery. For the IPO for Cerebras Systems for example, TradeXYZ simply had a Hyperp mechanism deriving the reference from the market’s own recent marks, and let the contract discover price in the narrow window between the S-1 and the listing. It worked better than anything else in the market. Launched May 1 at a $175 reference, CBRS traded $288-320 for two weeks and printed around $340 an hour before the open, within 3% of the $350 at which Nasdaq actually opened [9]. This estimate was roughly 84% above the $185 the bankers priced, and far more accurate than secondary brokers like Hiive ($225) and Forge ($113.50). This was a tremendous triumph for the perp as an instrument.

However, this process is not necessarily scalable, as clean discovery depended on an imminent, verifiable convergence event. Had Cerebras not listed within a certain time period, the contract would have settled to a TWAP of its own price. In this sense, the “perp price discovery” mechanism ended up looking like more like a traditional futures contract, and is also not necessarily scalable to earlier stage pre-IPOs that may not IPO anytime soon.

Thus, the design space for perp-based tokenized startups remains wide open. The scalable formula is yet to be written, and is likely one that blends together crypto perps with traditional futures, prediction markets, secondary spot markets, contracts for differences (CFDs) amongst other primitives. With Kalshi’s recent entrance into the perpetuals markets, and Hyperliquid’s entrance into outcome markets with HIP-4, we’re seeing a great convergence between all of these different pricing instruments. The pricing of tokenized pre-IPO startups could very well be the catalyst case for a novel derivatives landscape – one that is more efficient and accessible to the everyday user.

3.4 - Legal Structure and Regulation

From a legal structure perspective, many of these tokenized startup instruments, such as Street’s ERC-S, MetaDAO’s DAO LLC, and SPV-backed tokens are novel and experimental, and have not really withstood the test of time with a regulator with strict enforcement intent. Even the recent US CLARITY Act that addresses digital commodities does not address this question of tokenized equity.

From public statements, the SEC seems to bucket these tokenized startups into two distinct categories depending on whether the tokens are directly issued by the company or by third parties [13].

Issuer-sponsored tokens are the security itself, just re-formatted, and therefore are subject to traditional securities laws. Whether the official ledger sits on-chain (moving the token moves the share) or off-chain (the token triggers a books update), the treatment is identical to an ordinary share: register or qualify for an exemption, and carry every standard disclosure and reporting obligation.

Third-party tokens are treated by what they actually convey. A custodial token is a security entitlement under UCC Article 8 – a real securities transaction, but a claim on custodial shares rather than the shares themselves, which means you also absorb the custodian’s insolvency risk. A synthetic token is a wholly separate security issued by the third party, conveying no rights against the referenced company and requiring its own registration or exemption: linked securities (a note or SPV tracking the target’s value) sit here, while security-based swaps, such as the Ventuals-style perp, are the most constrained, barred from ordinary US retail unless both registered and traded on a national exchange.

Conclusion

Whether it be pre-IPO perps or SPVs, closed-end funds or secondary tenders, each of these instruments is an attempt to win back what public markets used to give away freely: early, liquid exposure to companies in their highest-velocity years, rather than let it get captured by growth equity funds.

Today, we know that the demand exists, but the infrastructure is yet to catch up. And for tokens, the stakes run deeper. The last few years have been an identity crisis: project tokens drifted into second-class citizenship, governance theater stapled to value that accrued elsewhere. Reinventing the IPO – giving the token a real claim on venture-scale upside –may be the generational mission that absolves it, returning the token to its ICO-era promise with the infrastructure the first wave never had.

Important Disclosures

This document is made available by Pantera Capital Partners LP (“Pantera”) for informational and educational purposes only. It does not contain all information pertinent to an investment decision. Nothing in this document constitutes an investment recommendation or an offer of investment advisory services. This document cannot be relied upon in making an investment decision. Nothing contained herein constitutes an offer to sell, or a solicitation to buy, any securities. This document contains information believed to be reliable, and has been obtained from sources believed to be reliable, but no representation or warranty is made (express or implied) of any nature, nor is any responsibility or liability of any kind accepted, with respect to the fairness, accuracy, completeness, or reasonableness of the information or opinions contained herein. Forward-looking statements should not be relied upon. There is no guarantee that investments in any instrument described herein will be profitable – all investments carry the inherent risk of total loss. Analyses and opinions contained herein (including market commentary, statements or forecasts) reflect the judgment of the author as of the date this document was published, and may contain elements of subjectivity (including certain assumptions) or be based on incomplete information. There is no duty or obligation to update the contents of this document. This document is not intended to provide, and should not be relied on for accounting, legal, or tax advice, or investment recommendations. Pantera and its principals have made investments in some of the instruments discussed in this communication and may in the future make additional investments or trading decisions in connection with such instruments without further notice. This document solely reflects the opinion of the author, and does not reflect Pantera’s opinions.

Past performance is not indicative of future results. Performance data cited for third-party platforms has not been independently verified and reflects specific periods that may not be representative of typical outcomes.

Investments in tokenized startup instruments involve substantial risk of loss, including complete loss of principal, regulatory risk, illiquidity, and absence of legal shareholder rights. These instruments are not suitable for all investors. Please consult qualified legal, financial, and tax advisors before investing.

References

[1]

[2] https://www.allocations.com/blog/what-is-an-spv-the-definitive-guide-to-special-purpose-vehicles

[3]

[4] https://www.hiive.com/market-reports/state-of-the-pre-ipo-market-2026-annual-report

[5] https://panteracapital.com/state-of-tokenization-q1-2026-pdf/

[6]

https://app.rwa.xyz/

[7] https://panteracapital.com/rise-of-perps-and-hyperliquid/

[8]

https://docs.trade.xyz/

[9] https://x.com/ArrakisFinance/article/2055338763442934205

[10]

[11]

[12] https://aurum.law/newsroom/Pre-IPO-Secondary-Tokenisation-After-Anthropic-and-OpenAI